Top 10 Takeaways from the 2020 Pharmacy Trend Report

“These [medical pharmacy] trends continue to be a challenge for all stakeholders involved in the care of patients with complex specialty conditions, making it vital for them to stay current and informed for better decision-making,” said Kristen Reimers, RPh, senior vice president, specialty clinical solutions, Magellan Rx Management.

Medical benefit drug spend, or what we call medical pharmacy, continues to be one of the largest cost drivers when it comes to overall specialty drug trends. At Magellan Rx, we have nearly 20 years of experience in managing this high-cost and complex portion of medical pharmacy spend and have published the industry’s only detailed source for trends related to medical pharmacy for the last 11 years.

Here are the trends you need to know from the eleventh edition of the Medical Pharmacy Trend Report:1

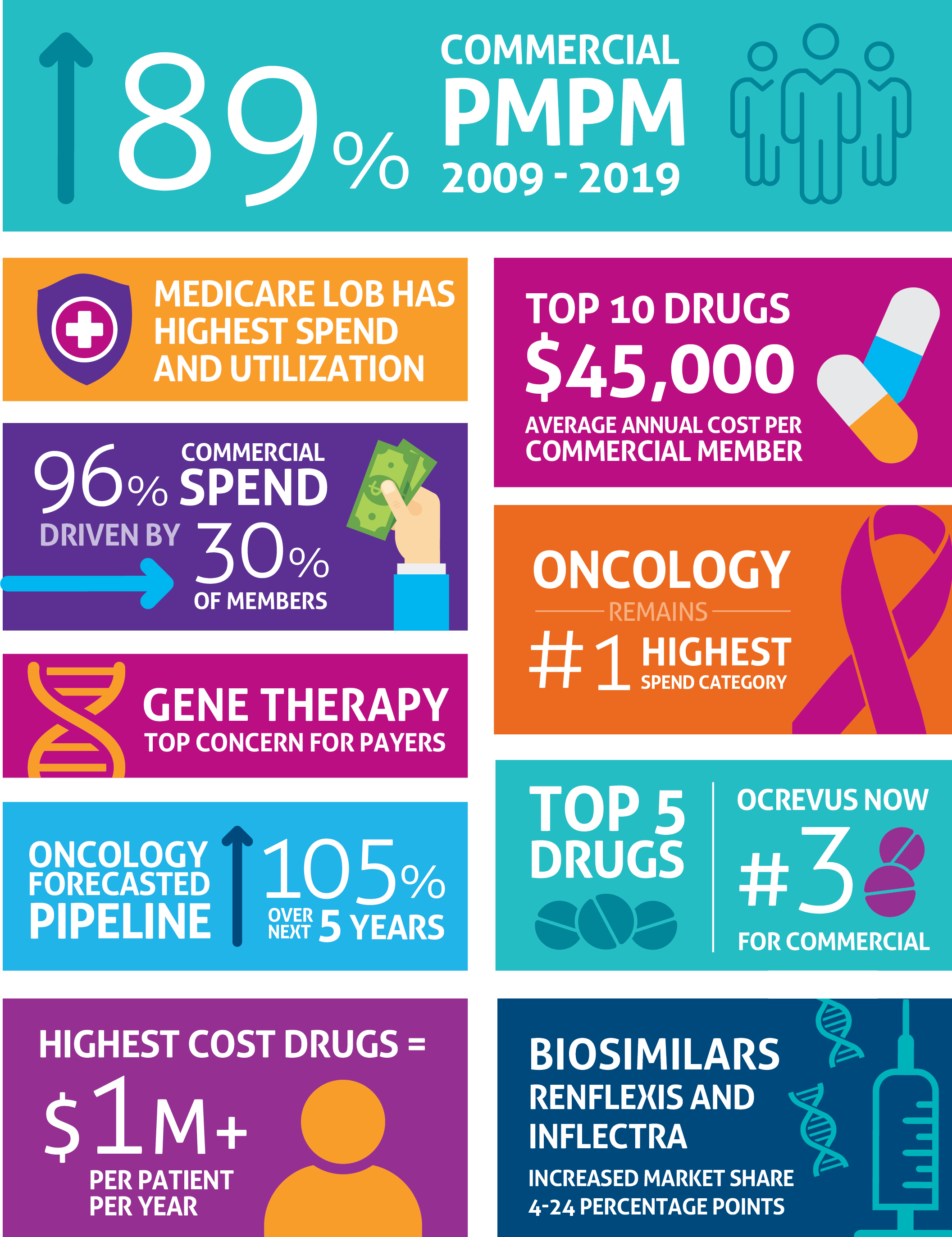

- Commercial per-member-per-month (PMPM) spend has increased 89% from 2009 to 2019.

- Medicare remains the highest spend and utilization line of business (LOB) with 10% of members having a medical drug claim.

- The average annual cost per member for the top 10 drugs is almost $45,000 for Commercial members.

- For medical specialty drugs 30% of members are driving 96% of the spend.

- Gene therapy is the top concern for payers in medical pharmacy.

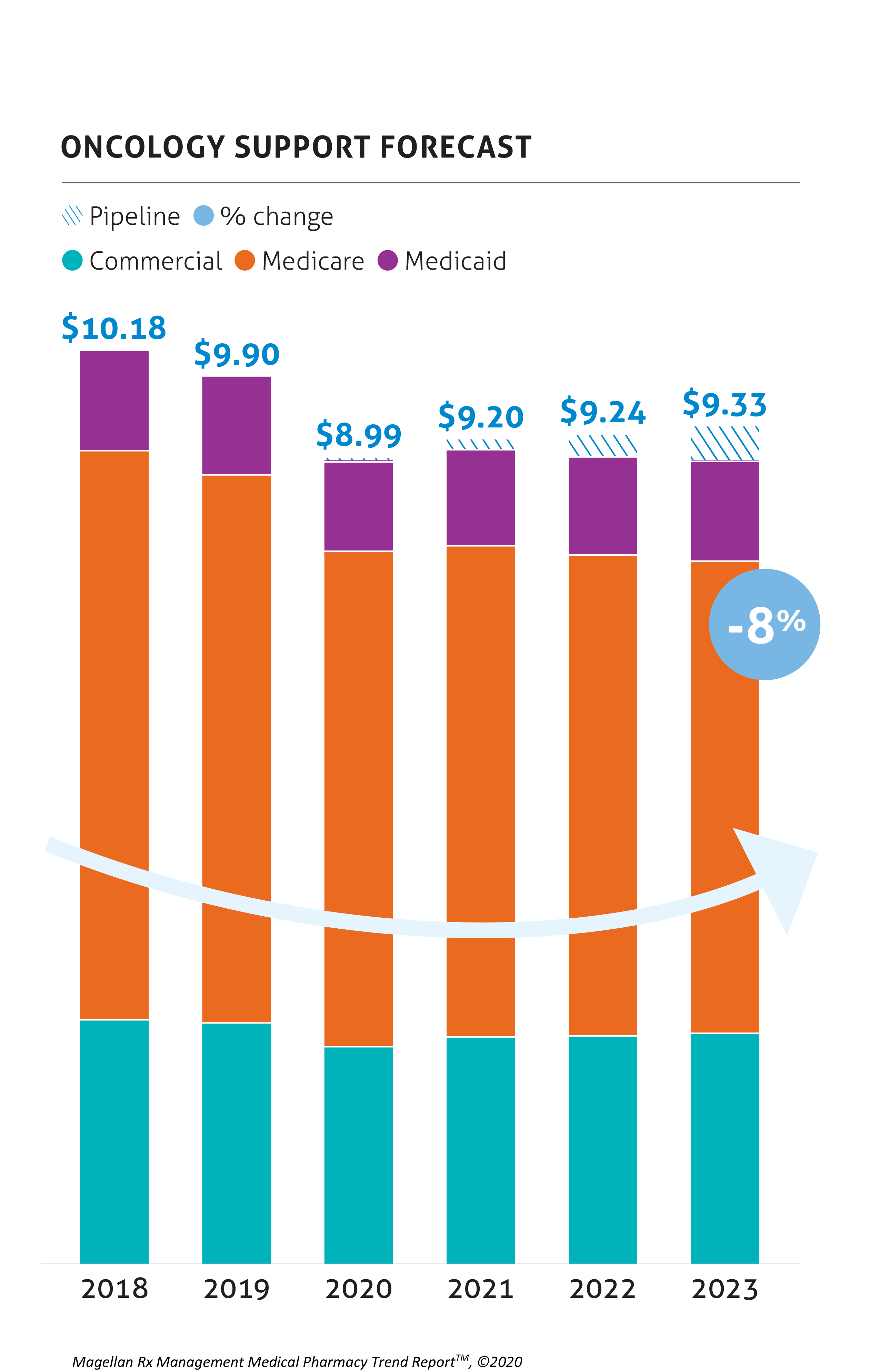

- Oncology remains #1 highest-spend category across all LOBs.

- The oncology pipeline is forecasted to increase 105% in PMPM spend from $52 in 2019 to $106 in 2024.

- There’s a new top five drug list for commercial: Remicade, Neulasta, Ocrevus, Herceptin, Avastin, with Ocrevus entering the top 5 and having an 85% trend.

- The highest-cost medical benefit drugs exceed $1M per patient per year.

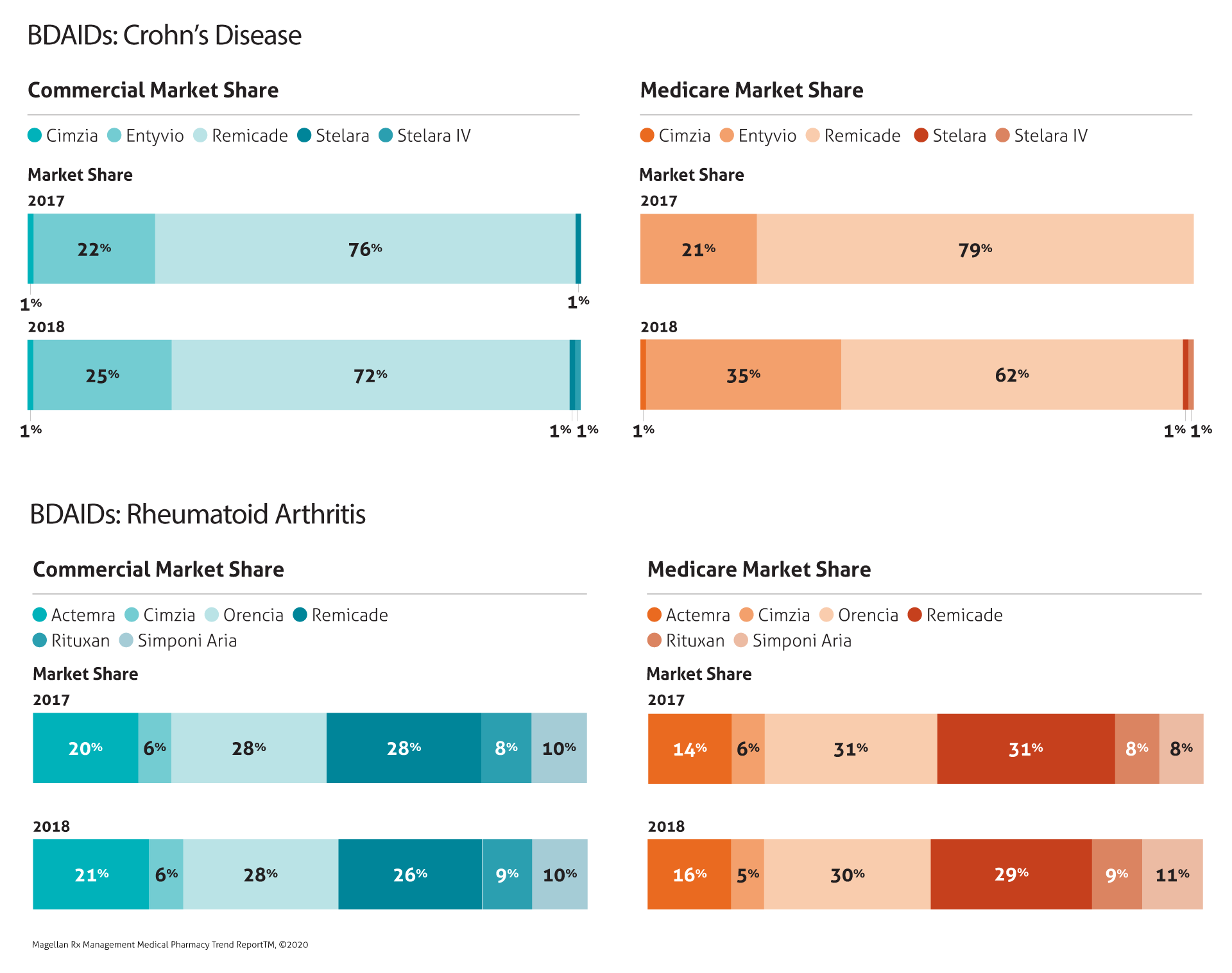

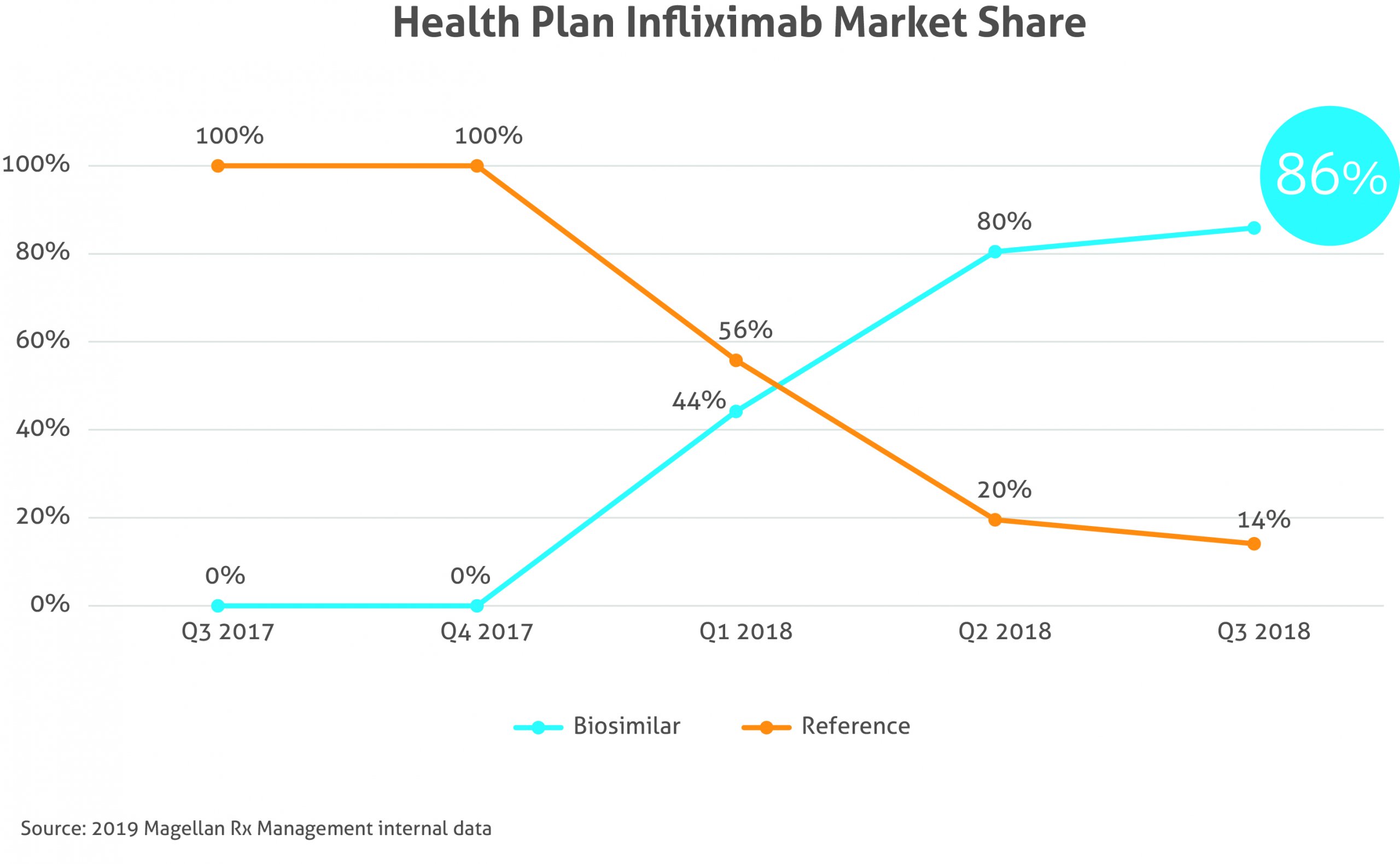

- Biosimilars Renflexis and Inflectra (in the BDAIDs category) market share increased 4-6 percentage points for commercial and Medicare and a substantial 24 percentage points for Medicaid.

Want to dig into these trends and more, including the latest in management strategies to combat rising pharmacy trend? Download your copy of the report.

- Unlock the Latest Trends and Emerging Strategies to Manage Rising Medical Benefit Specialty Drug Spend.” Magellan Rx Management Press Release, 20 May 2021. Accessed May 20, 2021.

- 2020 Magellan Rx Management Medical Pharmacy Trend Report™, © 2021.

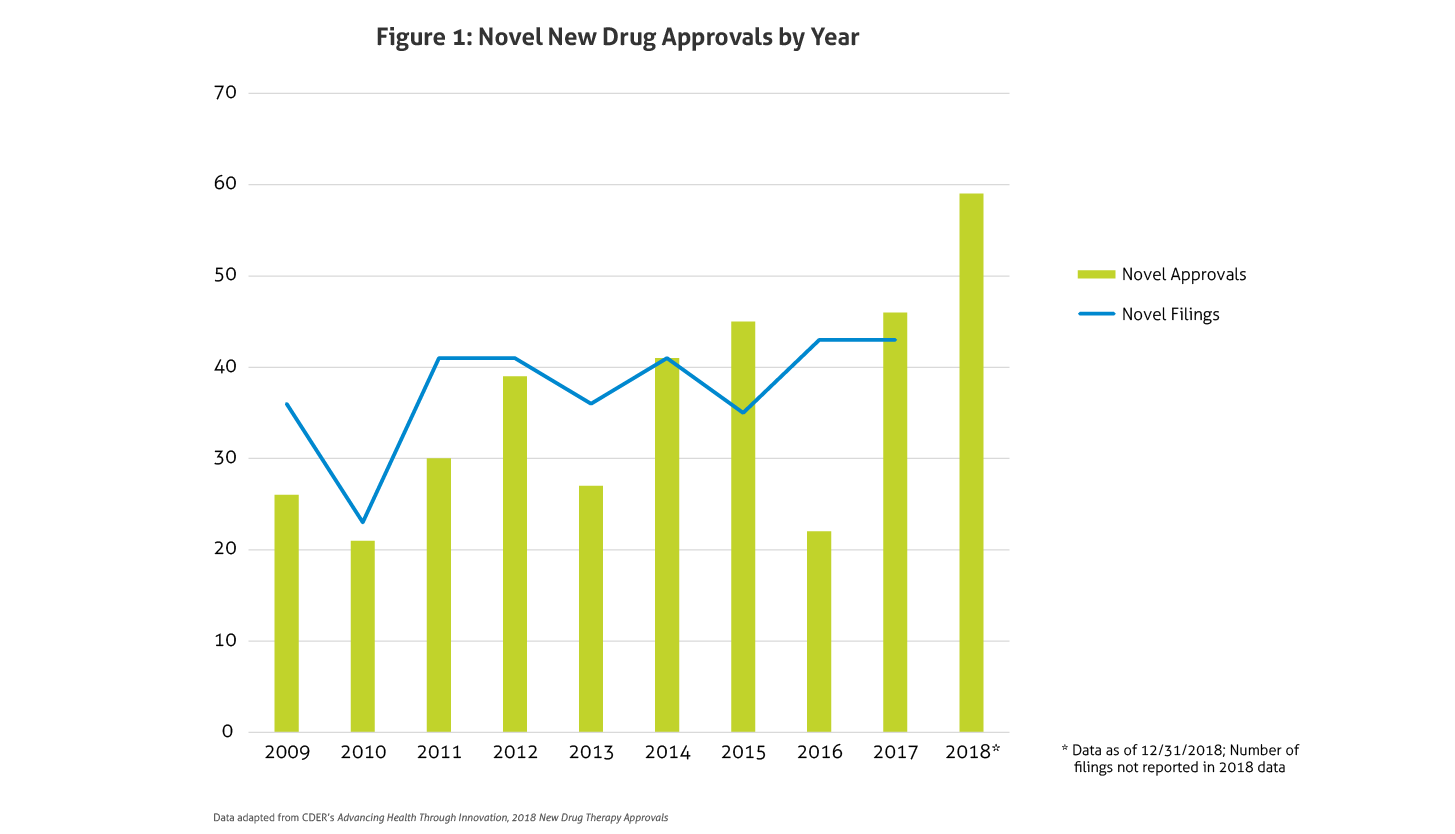

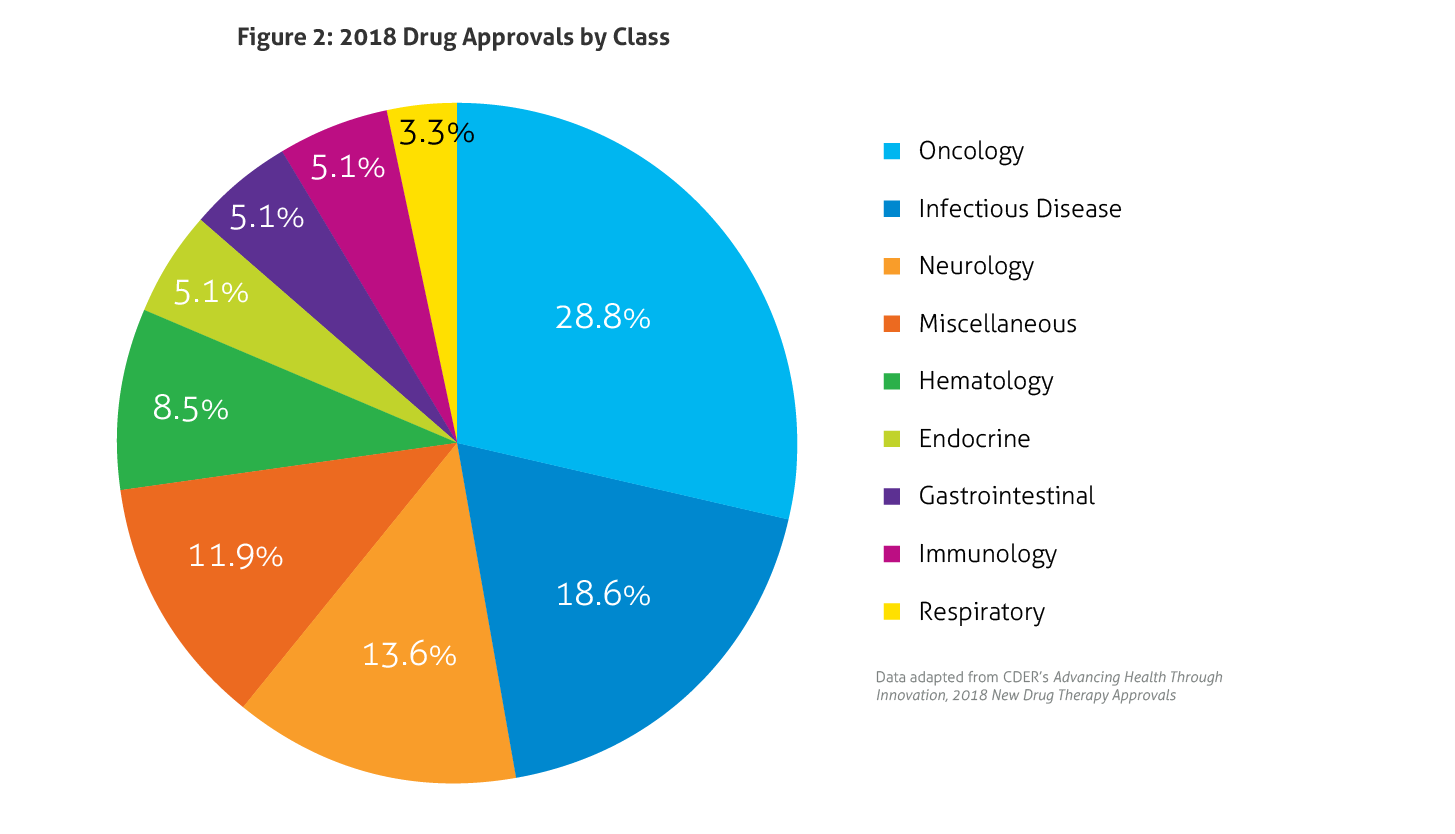

Some of the notable 2018 approvals included the first non-opioid drug approved to reduce opioid withdrawal symptoms, a new antiretroviral for multidrug resistant human immunodeficiency virus-1, a new class of drugs for migraine (calcitonin gene-related peptide receptor antagonists), the first FDA-approved drug derived from marijuana, the first treatment approved for multiple sclerosis in children, expanded options for cystic fibrosis, and the first antibiotic approved under the Limited Population Pathway for Antibacterial and Antifungal Drugs.

Some of the notable 2018 approvals included the first non-opioid drug approved to reduce opioid withdrawal symptoms, a new antiretroviral for multidrug resistant human immunodeficiency virus-1, a new class of drugs for migraine (calcitonin gene-related peptide receptor antagonists), the first FDA-approved drug derived from marijuana, the first treatment approved for multiple sclerosis in children, expanded options for cystic fibrosis, and the first antibiotic approved under the Limited Population Pathway for Antibacterial and Antifungal Drugs.